Back during the days of the Obama Administration, two claims were made about the budget:

- 2) Obama reduced US deficit levels

Oddly enough, both were true at the same time.

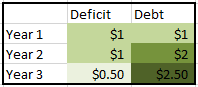

This is due to the debt and deficit being two distinct terms. The debt represents the total accumulated amount of money over budget and the deficit represents a yearly amount of money over budget.

To take an example: if in year 1 I spend $1 dollar more than I took in, I have a deficit of $1 and a debt of $1. In year two, if I also spend $1 dollar over my budget, I also have a $1 deficit, for year 2, but a new debt total of $2. If I then turn a new leaf for year 3 and only spend $0.50 more than I take in, my year 3 deficit is $0.50 and my debt will be $2.50, but I will have decreased my deficit in year 3 by 50%.

In other words, deficits are recurring phenomena and the debt is the total accumulated amount of all deficits (or surpluses) which occurred in the past.

Politicians and much of the media count on readers getting this wrong and thus use these two terms to reinforce their agendas. Obama’s supporters would tout his deficit decreases while his opponents would call him out for the increased amount of debt under his tenure. Both are correct, but what is key is recognizing these terms when they are used. It’s easy to get fooled and confused by deficits vs debts until this is understood.

With that in mind, enter the Tax Cuts and Jobs Act which was signed in 2017. The bill cut the corporate tax rate by 40%, raised the estate tax threshold (the amount the tax would kick in) by 100%, as well as additional cuts mostly favoring the wealthiest of earners (source: ). Such cuts have massive impacts on the federal budget, as will be shown, but this is likely by design of the bill’s key proponents.

Same Old Song and Dance

Proponents of the bill touted ‘trickle-down economics’ stemming from the Reagan Administration: cut taxes on centers of wealth (corporations/the wealthy/etc), and those centers of wealth will then trickle wealth down on the rest of society, thus to the benefit of all.

Treasury Secretary Steve Mnuchin said of the bill, “Not only will this tax plan pay for itself, but it will pay down debt,”. Senator Pat Toomey also mentioned that “I think this tax bill is going to reduce the size of our deficits going forward,”.

This strategy has proven to be a fraud again and again.

Trickle-down economics has such a dismal record that one wonders if it was simply an excuse cooked up in order to redistribute wealth to the top, consequences be damned.

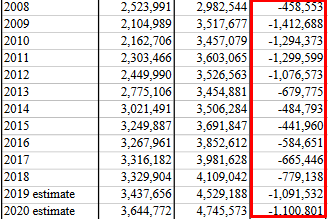

The consequences are starting to be seen. Take a look at historical deficits from the 2020 White House budget:

The Tax Cuts and Jobs Act largely took effect in 2018, and notice how quickly the deficits are expected to rise- likely in conjunction with one another. Causality is difficult to prove in such a large economy as ours, but it doesn’t take a genius to know that eliminating a big portion of revenue will result in higher deficits in the future.

Economist Richard Wolff discussed the tax cut bill back in 2018 and described that although some businesses did, in fact, increase employment slightly, much of the funds of the tax cut that corporations saved went to stock buybacks- or in other words payments to shareholders of stock.

And they wonder why our infrastructure is crumbling year after year.

A Manufactured Crisis

To summarize quickly in stark terms: a tax cut bill was recently passed resulting in higher deficits, which are rising significantly, thus growing the debt each year. Add to that significantly increased military spending, and we have a budget problem on our hands. A budget problem in the middle of one of the largest periods of economic recovery in US history.

It almost seems like this was planned all along: redistribute wealth to the top and use the resulting deficits to cut social and other government programs for everyone else. Rebekah Entralgo has put together some Congressional opinions of the tax bill’s proponents shortly after it took effect, exposing the game plan on this (bold is mine):

- Paul Ryan, then Speaker of the US House of Representatives: “We’re going to have to get back next year at entitlement reform, which is how you tackle the debt and the deficit”

- Pat Toomey, US Senator: “We’ve got entitlement spending that is not sustainable. These big spending programs that are growing faster than the economy. You can’t tax your way out of that problem. You’ve got to make some curbs”

- John Thune, US Senator: “If we’re going to do something about spending and debt, we have to get faster growth in the economy — which I hope tax reform will achieve. But we have also got to take on making our entitlement programs more sustainable. I think there is support, generally, here for entitlement reform.”

- Tom Cole, US Representative: “If someone wants to get serious about debt, come talk to me about entitlements. Tax cuts produce growth, entitlement spending doesn’t.”

Bryce Covert writes:

“But now that they’ve succeeded in passing a tax package that will reduce government revenues so much, the ensuing cost will serve as the excuse to get everything else they want. They’ll count on our short memories to forget who created larger deficits in the first place. Those deficits will serve as the motivation to enact cuts they’ve sought all along. The tax bill isn’t just a regressive giveaway to corporations and the rich. It’s a Trojan horse with deep government reductions stuffed inside.”

Blowing a hole in the deficit is likely going to force negotiations over cuts to Medicare, Social Security, and Medicaid (among others), and the prospects don’t look good for the working class. Look out for this coming budget battle to play out in the next year or so.

What can be done?

What is needed is comprehensive tax reform to reverse the decades long trend of income redistribution from the poor and working class and a shift of that tax burden more towards the centers of power and wealth in this country. It’s been done before, via of the New Deal.

Drastically reducing the military budget is another necessity, as the US spends an absurd amount on its military compared to the rest of the world. Multiple studies have been conducted (here and here) concluding that the US has spent between $4-$7 trillion in Middle East wars since 2001.

Candidate Trump, as opposed to President Trump, in 2016 stated: “We’ve wasted $6 trillion in wars in the Middle East. We could have rebuilt our country twice”. Many times when proposals arise for social programs to benefit workers, the common ‘how are you going to pay for it?’ question arises. Almost never will a reader hear it for wars and military spending, though, and where has our trillions spent in the Middle East gotten us?

Add up the reportedly $1 trillion spent on the War on Drugs, the hundreds of billions spent subsidizing fossil fuels, the $700 billion bank bailout in 2008, the tax cut bill mentioned already, and the recent audit of the Pentagon from 1998-2015 which resulted in trillions of dollars unable to be accounted for, and readers can get the picture of what is going on.

For these programs, the narrative wasn’t ‘how are you going to pay for that?’ because they benefit wealth and power. Credence Clearwater Revival put it well in their song Fortunate Son:

Some folks are born, silver spoon in hand

Lord, don’t they help themselves, y’all

But when the taxman comes to the door

Lord, the house looks like a rummage sale

The question is not whether the money is there, it’s instead how it’s going to be spent, and for what purpose?

A mandate from the poor and working class is necessary. Only then will the budget be accommodated enough to warrant the infrastructure, social, and other spending that is sorely needed. Such a program like the New Deal could take decades to put into fruition, but one key element will be banking and monetary policy.

Readers may find banking and monetary policy to be a bore but it’s vital to understanding our economics.

A recent development in money and banking has emerged called Modern Monetary Theory (MMT). Readers can listen to a description of it here and here and read a debate about this controversial theory here and here from both a skeptic and proponent of MMT.

In short: MMT focuses on governments that can issue their own currency or have it done for them via a central bank (the Federal Reserve, in the case of the US). For these governments, the central bank can create money to pay for things such as government programs, avoiding default, and the promotion of full employment, among others. The old concept of governments being constrained by debts and deficits is outdated, MMT theorists claim, since a central bank can create money for services it deems fit.

If a central bank creates too much money to result in inflation, the central bank can then recover money back from the economy in the form of taxes and selling assets, thus balancing the previous spending.

MMT, proponents would argue, is one way to fund such an ambitious- and needed- social program like a New Deal 2.0, or Green New Deal, as was recently introduced by Representative Alexandria-Ocasio Cortez.

A Discussion with Economist Richard Werner

But MMT has its skeptics and opponents. Richard Werner, economist, professor, and author of Princes of the Yen which has also been made into a documentary, has been kind enough to provide his insight into Modern Monetary Theory regarding its viability and practicality.

Q: With new discussion around Modern Monetary Theory (MMT) and its seeming usefulness to highlight the ability of central banks to buy up bad debt in exchange for fresh monetary reserves (similar to what happened with the Bank of Japan after WWII), is such a reality desirable in the US if, for example, sufficiently high national debt coupled with a crippling recession were to occur?

Werner: After 1945, the Bank of Japan did not buy up national debt, but instead it bought the non-performing assets from the banks in order ensure they can increase bank credit creation again and thus cause an economic recovery. This worked well. I wrote about it here.

I advised such action in the 1990s in Japan, a discussion that Ben Bernanke participated in. The Federal Reserve Bank of New York in fact did do this in October 2008, which is why bank credit creation recovered very quickly.

However, it should be noted that the Federal Reserve Bank of New York is 100% privately-owned and thus not directly subject to government control. Consequently, this new theory once again remains in the theoretical dream world that economics seem to have retreated to long ago.

Instead of more theoretical economics that is removed from economic reality, I strongly recommend Scientific Economics, which is the new branch of economics I have been building up. I contend that there is no good reason not to use the scientific research method also in economics. I know, it is radical and most economists – mainstream and unorthodox – hate the idea that empirical reality should be more important than their preferred fancy ideas, ‘axioms’ or other wishful thinking devised by some guru they admire.

Moreover, it is worth mentioning that my original definition of ‘Quantitative Easing’ – then a new monetary policy, which I proposed in 1994/1995 in Japan – was defined as increasing bank credit creation for the real economy (GDP transactions), which can be achieved, among other measures, by the central bank purchasing the banks’ non-performing assets to clean their balance sheets. This does not use tax payers’ money and hence does not increase national debt. It also does not create money and hence cannot result in inflation. My proposal is based on the Quantity Theory of Disaggregated Credit, which solves the empirical puzzles found in the other schools of thought in macroeconomics (see e.g. here or here)

For other measures to stimulate the economy after a banking crisis, even with a non-cooperative (independent) central bank, see my other policy proposal called ‘Enhanced Debt Management’ explained in detail here.

Q: Regarding your original Quantitative Easing policy relating to a given central bank purchasing such assets: am I correct in stating that although it wouldn’t involve tax payer money, it would still contribute to inflation, but only slightly? I ask because as I understand it, such activities of central banks, or at least in the US, account for only a small portion of money creation in the economy- the largest portion coming from fractional reserve lending via commercial banks.

Werner: No, central bank purchases of the non-performing assets from the banks’ balances sheets would not involve any inflation. Quite impossible. So if a central bank thought that with this policy they can generate inflation, it’s a big mistake.

Proof: The Fed purchased the non-performing assets from the US big banks and even insurance companies, quadrupling its balance sheet within one month. No inflation. No weakening of the dollar.

Explanation: As I argued when I proposed this in the early 1990s, central bank purchases of assets from banks does not involve money creation. Money creation takes place when the money creating parts of the system inject new purchasing power into the rest of the economy. The central bank and banks make up the banking system, which is the money creating part of the economy. Any transaction within this money creating part, such as between the central bank and the banks, has no direct impact on the rest of the economy. Since no new money is directly injected as a result of this transaction into the non-banking economy, there cannot be inflation.

Q: You mentioned that the Federal Reserve is privately owned and thus the benefits of MMT when it comes to stimulating or recovering an economy is purely theoretical.

But given a movement of sufficient popular pressure or legislative reform, and notwithstanding (or even in conjunction) with your prescription for bank-to-bank operations already discussed, in your view is it possible that on a national level the Federal Reserve could be compelled to act in such a way that MMT advocates argue for? Namely by using the Federal Reserve coupled with fiscal policy to, for example, boost employment, provide services, etc.

If a central bank could be compelled to act in such a way (and given the immense difficulty of achieving this due to their independence), it seems to me analogous to Japan’s Window Guidance program only on a national level.

Werner: I think we are called to analyse the situation in the current institutional setting. Changing the setting as a basis of analysis makes it far more hypothetical and theoretical. But if we do engage the political process to change the setting, then nationalising the Fed or, as Milton Friedman recommended, incorporating the Fed into the US Treasury, would be a good next step. But simply – and counter-factually – assuming this has already happened is counter-productive.